Shares of eBay Inc. (NASDAQ: EBAY) stayed green during afternoon trade on Friday. The stock has gained 34% over the past three months. The ecommerce company delivered strong results for the second quarter of 2025 as it remained resilient against an uncertain macroeconomic backdrop. This performance was driven largely in part by momentum in its focus categories.

Major growth engine

As mentioned on its quarterly conference call, focus categories continue to be a significant growth engine for eBay. In Q2 2025, focus category gross merchandise volume (GMV) grew by over 10%, with broad-based growth across all individual focus categories compared to the year-ago period.

The collectibles category was the biggest contributor to this growth, led by momentum in collectible card games and sports trading cards. Pokemon cards have seen a rise in popularity thanks to renewed interest from collectors and a strong slate of product releases, leading to triple-digit growth in GMV. The company continues to see strong growth in all its major trading card subcategories.

The momentum in collectibles was also helped by eBay’s strategic initiatives, which include grading solutions, bulk selling capabilities, and expanding its inventory and offerings for collectors. Motors Parts and Accessories, and luxury and apparel-focused categories also contributed meaningfully to GMV growth in the second quarter.

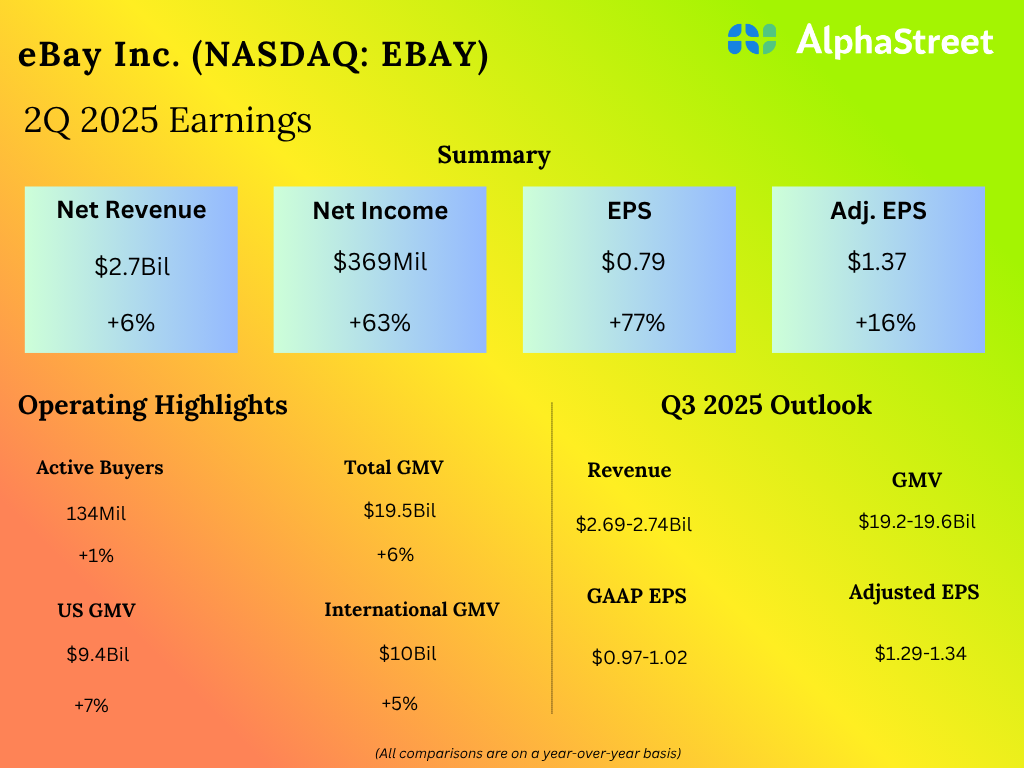

Results led by resilience

In Q2 2025, eBay reported growth in revenue, GMV and earnings, driven by its strategic initiatives. The quarterly performance was also helped by improved consumer demand in the US as well as a more subdued impact from tariffs than expected.

Net revenues increased 6% year-over-year to $2.7 billion on both a reported and FX-neutral basis. GMV grew 4% on an FX-neutral basis to $19.5 billion. Adjusted earnings per share rose 16% to $1.37.

Outlook

eBay continues to see favorable consumer trends in the US even in a dynamic environment. For the third quarter of 2025, the company expects to see 3-5% YoY growth in both revenue and GMV on an FX-neutral basis. Revenue is forecast to range between $2.69-2.74 billion while GMV is expected to range between $19.2-19.6 billion. Adjusted EPS is expected to be $1.29-1.34.

EBAY expects the strength in focus categories to continue through the remainder of the year. For the full year of 2025, it anticipates GMV to come in slightly above the previously expected range of low-single-digit FX-neutral growth.

Meanwhile, the company expects GMV to be impacted by a couple of factors such as tough YoY comparisons due to a strong holiday season and some potential moderation in trading cards growth during the fourth quarter, lapping an acceleration in UK C2C volume, and impacts from tariffs and new trade policies. EBAY forecasts revenue growth to be modestly higher than GMV for the full year on an FX-neutral basis.