Micron Expertise Inc. (NASDAQ: MU) is gearing as much as report first-quarter outcomes after delivering a robust efficiency within the remaining months of FY25. Because the main reminiscence producer within the US, the corporate is well-positioned to capitalize on the accelerating AI alternative. The momentum is fueled by surging demand for Excessive Bandwidth Reminiscence, a crucial element in next-generation AI infrastructure.

What to Anticipate

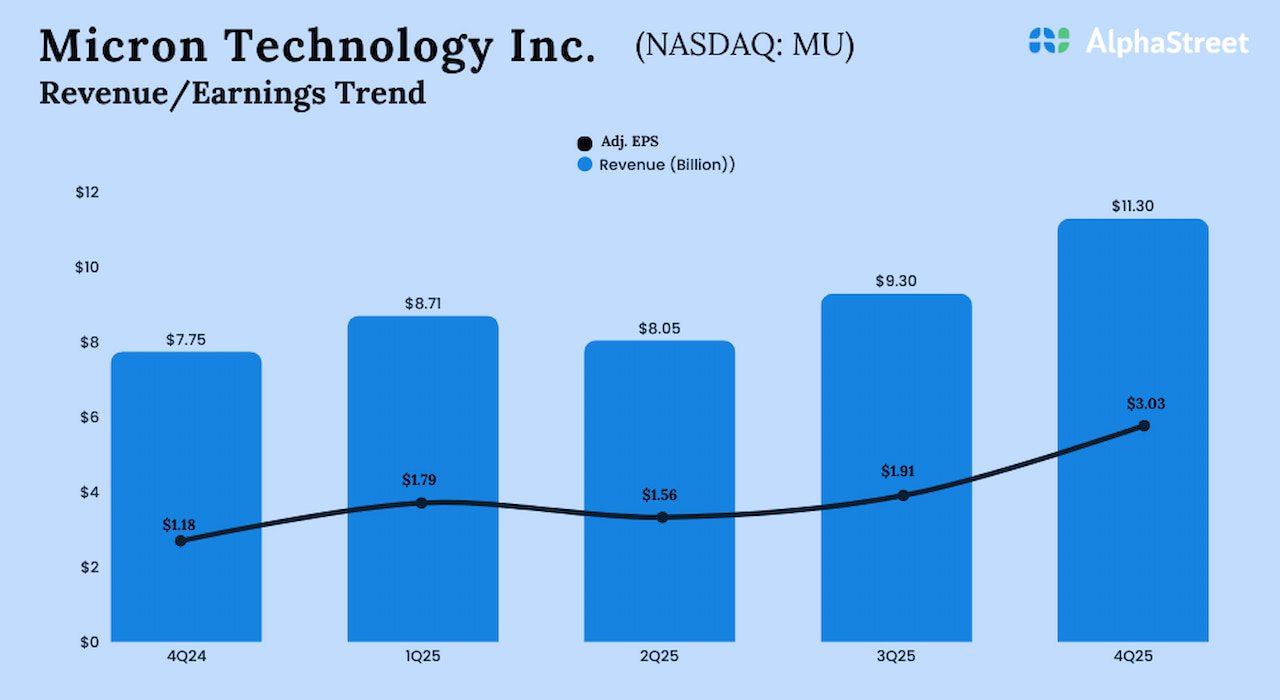

Within the latest assertion, the Idaho-headquartered tech agency mentioned it expects first-quarter 2026 revenues to be round $12.50 billion, and adjusted earnings to be roughly $3.75 per share. The projection is under analysts’ estimates for revenues of $12.71 billion and earnings of $3.83 per share for the quarter. Notably, within the comparable quarter of FY25, the corporate posted a a lot decrease income of $8.71 billion and earnings of $1.79 per share. The Q1 report is scheduled for launch on December 17, after common buying and selling hours.

Over the previous three months, Micron’s inventory has been in an upward spiral, greater than doubling and outperforming the S&P 500 index by a large margin throughout that interval. A number of weeks in the past, the shares climbed to an all-time excessive earlier than ending the rally and stabilizing forward of subsequent week’s earnings. The upbeat investor sentiment primarily displays the energy of Micron’s knowledge middle enterprise, with revenues reaching all-time highs throughout the board in fiscal 2025. Regardless of the elevated valuation, in comparison with historic averages, Micron stays a compelling long-term funding.

Earnings Surge

Within the fourth quarter, adjusted earnings greater than doubled year-over-year to $3.03 per share, beating estimates. On a reported foundation, internet revenue was $3.20 billion or $2.83 per share in This autumn, in comparison with $887 million or $0.79 per share within the prior-year quarter. Driving the bottom-line progress, revenues rose sharply to a file excessive of $11.3 billion from $7.75 billion final yr, exceeding expectations. Quarterly income and revenue have persistently crushed estimates since Q3 2023. Buoyed by the sturdy This autumn consequence, the Micron management raised its progress forecast on industry-DRAM-bit demand and industry-NAND-bit demand for calendar 2025.

From Micron’s This autumn 2025 Earnings Name:

“As we enter fiscal 2026, Micron is positioned higher than ever. Our management in superior applied sciences, together with HBM, 1-gamma DRAM, and G9 NAND, permits a differentiated product portfolio that drives sturdy ROI. AI-driven demand is accelerating, and {industry} DRAM provide is tight. Our HBM efficiency has been sturdy, and sturdy demand, tight DRAM provide, and disciplined execution have considerably strengthened the profitability of the remainder of our DRAM portfolio. In NAND, our greater combine to knowledge middle and enhancing {industry} situations are contributing to profitability. Our fiscal Q1 steering displays new data for income and EPS.”

AI Increase

There was a extreme scarcity of reminiscence globally, because the AI-driven progress within the knowledge middle has led to a surge in demand for reminiscence and storage. Earlier this month, Micron revealed plans to exit its client reminiscence enterprise to enhance provide and assist for bigger prospects in faster-growing segments. The administration targets fiscal 2026 CapEx above its FY25 spending of $13.8 billion as the corporate continues to speculate closely in superior DRAM expertise and Excessive Bandwidth Reminiscence.

Micron’s inventory value has greater than tripled because the starting of 2025, and is buying and selling properly above its 12-month common worth of $127.03. MU was up 2.3% on Tuesday afternoon.