For Intel Company (NASDAQ: INTC), 2025 marked a restoration 12 months, as the corporate made notable progress in direction of reaching its technological and operational milestones. After dropping important market share to rivals lately, the corporate is on the lookout for a resurgence. It’s actively working to leverage the AI-driven surge in compute demand by increasing its portfolio and manufacturing footprint.

Cautious View

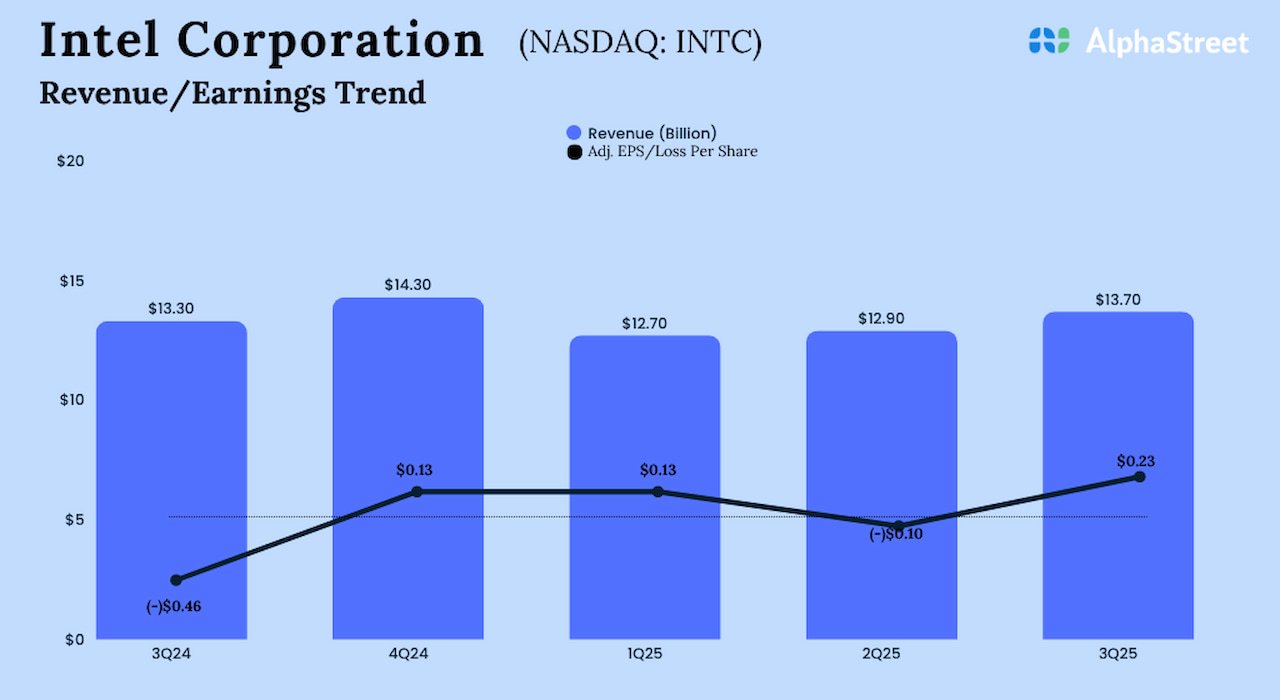

It’s estimated that the tech behemoth delivered a modest efficiency within the ultimate months of FY25. Wall Avenue analysts anticipate fourth-quarter earnings to say no to $0.08 per share, adjusted for one-off objects, from $0.13 per share within the corresponding quarter of the prior 12 months. The forecast for This autumn income is $13.37 billion, vs. $14.26 billion final 12 months. The corporate has scheduled the earnings announcement for January 22, after common buying and selling hours.

Over the previous six months, Intel’s inventory worth has practically doubled, considerably outperforming the broader market after buying and selling principally sideways in early 2025. Nevertheless, the latest closing worth stays properly under the inventory’s peak. It seems that traders are optimistic about Intel’s development technique, which facilities on ramping up its foundry enterprise and is supported by massive investments from the U.S. authorities and massive firms akin to Nvidia and Japan’s SoftBank.

On Restoration Path

Within the third quarter, Intel’s income elevated 3% from final 12 months to $13.65 billion. Shopper Computing income rose 5%, whereas Knowledge Middle and AI income declined 1%. On a per-share foundation, earnings got here in at $0.23 within the September quarter, excluding particular objects, in comparison with a lack of $0.46 per share within the year-ago quarter. On an unadjusted foundation, internet revenue was $4.06 billion or $0.90 per share, in comparison with a lack of $16.6 billion or $3.88 per share in Q3 2024. Each revenues and earnings topped Wall Avenue’s expectations.

From Intel’s Q3 2025 Earnings:

“We’re nonetheless within the early phases of the AI revolution, and I consider Intel can and can play a way more important position as we remodel the corporate. This begins with our core x86 franchise, which continues to play a important position within the age of AI. AI is clearly accelerating demand for brand new compute architectures, {hardware}, fashions, and algorithms. On the identical time, it’s fueling renewed development of conventional compute because the underlying knowledge and the ensuing insights proceed to rely closely on our current merchandise.”

Tech Ramp

The US authorities has supplied substantial monetary help to Intel as a part of efforts to advertise the home manufacturing of superior microchips, lowering reliance on Asia-based suppliers akin to Taiwan Semiconductor Manufacturing Firm. Whereas the corporate seems to be to profit from sturdy data-center demand from massive enterprises this 12 months, the first wager is on its superior semiconductor manufacturing course of node, 18A. Claimed by Intel to be the primary actually superior course of node manufactured at scale in the US, preliminary shipments of 18A-based merchandise started final 12 months.

On Tuesday, Intel’s inventory opened at $45.89, which is sharply increased than its 12-month common worth of $26.87. The shares have gained a formidable 22% up to now 30 days.