Each digital exercise leaves a bodily path. While you make a UPI fee, stream Netflix, again up WhatsApp, place a inventory market commerce or ask ChatGPT a query, that request travels to a knowledge centre, the place servers course of it and ship a response again in milliseconds. As soon as seen because the Web’s invisible plumbing, information centres are actually on the centre of a world infrastructure increase pushed by AI, cloud computing and surging digital site visitors.

The info centre business makes use of an uncommon conference: Though operators are successfully digital landlords renting out house and computing capability, amenities are sized and marketed by {the electrical} energy accessible to IT tools, expressed in MW or GW of “IT load”, moderately than by flooring space, server depend or information dealt with. Actual property marketing consultant Knight Frank estimates information centre international stay IT capability at about 60 GW in 2025, rising to over 93 GW in 2027, whereas one other marketing consultant JLL sees as a lot as 100 GW of recent capability by 2030.

The worldwide rush has been extraordinary, and information centres are altering with it. AI amenities want way more energy, cooling and electrical infrastructure than older ones, as massive language fashions can require 10-100 instances the computing energy of conventional functions. By 2030, AI may account for half of all computing exercise, with operating skilled AI fashions driving most of it.

That template is now taking part in out in India too. Regardless of producing an estimated 20 per cent of the world’s digital information, our information centre market stays far smaller than these of the US or China, although it’s among the many fastest-growing, with capability rising from about 0.375 GW in 2020 to round 1.5 GW by 2025 (estimated 130-150 energetic information centres). Mumbai and Chennai account for a lion’s share of put in co-location capability as we speak due to their proximity to sub-sea cable touchdown stations. Projections counsel a three-seven-fold rise in nationwide capability by 2030, to 4.5-10 GW. Hyperscalers (usually massive cloud suppliers), resembling AWS, Microsoft, Google and Oracle, already account for greater than half of India’s information centre IT capability, with BFSI and IT & Telecom being the opposite main shoppers.

Under, we unpack information centre evolution, enterprise, economics and alternatives.

Transient historical past of knowledge centres

Knowledge centres have advanced consistent with the altering wants of computing. Their origins might be traced to the Nineteen Forties and Nineteen Fifties, when early mainframe computer systems had been so massive and power-intensive that they required devoted rooms with specialised cooling. One of many earliest examples was the U.S. Military’s ENIAC, accomplished in 1945 on the College of Pennsylvania.

Within the Sixties and Seventies, as companies more and more adopted mainframe methods, devoted laptop amenities turned extra widespread. IBM helped speed up this shift within the Seventies by growing standardized websites for its mainframe machines, supporting the rising want for large-scale information processing.

The Nineteen Eighties marked a serious transition with the rise of client-server structure. Organizations now wanted separate areas not just for servers but in addition for networking tools, laying the groundwork for the fashionable information centre as IT assets turned extra centralized.

Demand expanded sharply within the Nineteen Nineties with the expansion of the web. Corporations wanted dependable infrastructure to host web sites and run on-line providers, resulting in speedy enlargement in information centre capability.

Within the 2000s, virtualization improved server utilization and helped pave the best way for cloud computing. Knowledge centres turned extra scalable and versatile, remodeling how companies deployed infrastructure and managed digital operations.

The 2010s noticed the emergence of hyperscale information centres constructed to deal with the huge processing and storage wants of expertise giants. On the similar time, edge computing started gaining floor by shifting processing nearer to customers, serving to cut back latency and enhance efficiency.

Within the 2020s, information centres are being reshaped once more by synthetic intelligence, which calls for far larger computing energy. Alongside this, sustainability has develop into a central precedence, with operators focusing extra on lowering vitality use and decreasing environmental influence.

Not only a constructing of servers

A go to to a contemporary information centre feels much less like getting into an workplace and extra like getting into a army facility: Armed guards, a number of biometric checks and man-trap doorways exterior, adopted by lengthy, deafening corridors of blinking server racks, thick cables and icy air inside.

At its core, a contemporary information centre is 5 issues rolled into one. A safe constructing that homes servers and storage, a non-public electrical energy system with a number of layers of backup, a cooling system designed to take away large quantities of warmth, a community hub linked to fibre-optic cables and the broader Web, and computing energy from central processing items (CPUs), graphics processing items (GPUs), and specialised chips.

In accordance with BofA World Analysis, IT tools (servers, networking, storage) accounts for 79 per cent of the fee, adopted by engineering, contractor, constructing and set up prices (E&C) at 11 per cent, electrical tools at 5 per cent, thermal or cooling tools at 4 per cent and backup diesel mills at 1-2 per cent.

Conventional information centres are constructed on-site and expanded step by step, making them slower to deploy however extra customisable. Modular amenities, in contrast, use prefabricated items that may reduce development time from roughly 18-24 months to 6-12 months.

However the quicker information centres scale, the tougher it turns into to disregard their side-effects. Past land and capital, these amenities place heavy calls for on energy grids, water assets and native infrastructure.

Totally different fashions

Knowledge centres can broadly be understood by means of 4 fashions, although these classes typically overlap.

Captive or enterprise information centres are owned and run by an organization for its personal workloads. A financial institution, inventory alternate or massive enterprise could desire this route for tighter management over safety, compliance and design. The trade-off is excessive capex, decrease flexibility and the burden of managing energy, cooling and safety in-house.

Co-location (colo) information centres are shared amenities the place a number of clients lease house, energy and connectivity from an operator resembling Equinix or Digital Realty. They cut back upfront prices and enhance scalability however supply much less management than captive set-ups and go away customers depending on operator uptime and pricing. In India, the common colo capex per MW in India is ₹46.5 crore/$5.4 million and this works out to roughly ₹24,200 of capex per sq ft, per JM Monetary. Analysis by Soben (a part of Accenture) discovered that cloud information centres at the moment value between $8 million and $10 million per MW, GW+AI information centres are costing as a lot as $17 million per MW. This hole displays variations in scope, geography, design assumptions, and included IT and {hardware}.

Hyperscale information centres refer extra to measurement and depth than possession. These are big campuses constructed for cloud majors resembling Amazon, Microsoft, Google and Meta, both for their very own use or by means of leased capability from operators. They’ll vary from a number of dozen MW to 100 MW-plus at a web site degree, with some campuses deliberate at far bigger scale. They ship scale and effectivity, however require large energy, land and capital. A more moderen variation of this buildout is CoreWeave, which is nearer to an AI-focused leased-infrastructure mannequin constructed round GPU cloud workloads.

Edge information centres are smaller, decentralised amenities positioned nearer to customers and gadgets, typically beneath 10 MW in India, together with in smaller cities and cities. Telecom operators use such set-ups to chop latency and assist real-time functions, although these websites normally supply decrease redundancy and uptime than massive centralised amenities.

Curiously, current assaults on information centres and digital infrastructure throughout the Center East battle have revived curiosity, no less than in idea, in underground and even space-based amenities. However each stay prohibitively costly: underground campuses can value 1.5-2 instances as a lot as standard ones, whereas Deutsche Financial institution Analysis estimates a 1 GW house information centre would value no less than seven instances greater than a terrestrial one.

Enterprise economics

Knowledge centres generate income by means of pricing fashions primarily based on rack items (server slots), full racks (complete cupboards), cages (non-public enclosed areas) and different codecs, with pricing more and more linked to the quantity of energy allotted to them. Charges rely on location, energy availability, community density, uptime, safety and contract construction. Pricing also can fluctuate by buyer measurement, starting from retail customers taking below 0.25 MW to hyperscalers taking above 4 MW.

Retail and wholesale colo contracts usually run for three-five years, whereas hyperscaler offers normally final no less than 5 years and may prolong to 10.

Broadly, there are two income fashions. Within the dominant lease mannequin, the information centre operator rents out house, energy and cooling, whereas the client manages its personal IT infrastructure. In managed providers, the operator additionally offers cloud or IT infrastructure and costs on a utilization foundation. In India, lease leases might be round ₹10-11 crore per MW per 12 months, with utilities usually handed by means of individually.

Apart from pricing and capability, a knowledge centre’s profitability is dependent upon occupancy and price management.

In India, colo occupancy has climbed sharply, from 82 per cent in FY20 to 97 per cent in FY25. With amenities now operating at 95-97 per cent occupancy, contemporary capability additions have gotten more and more important.

On pricing, probably the most helpful present benchmark is realised rack price, which Jefferies estimates at an combination ₹7,428 per kW per 30 days in FY25. Month-to-month pricing, usually, falls as buyer measurement rises.

Energy is the single-most important useful resource for information centre operations and a important think about monetary viability. Due to renewable energy, India will not be wanting electrical energy in combination. However that doesn’t robotically imply each location has simple, dependable and scalable entry to it. Tariff classification issues, since information centres normally search industrial energy charges, which might be materially decrease than industrial tariffs.

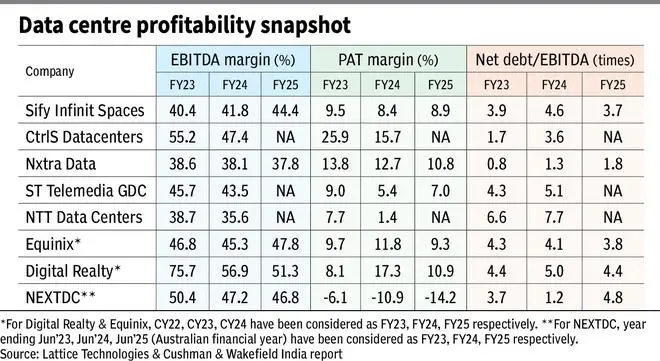

Change in vitality prices can hit or profit reported EBITDA margins (FY25: of 37-44 per cent for gamers in India and 47-51 per cent for international corporations). Energy density has elevated because of GPUs, which are actually central to fashionable computing, particularly in AI, information analytics, and high-performance computing. For context, NVIDIA H100 and H200 GPU-based racks usually draw about 10-30 kW every, marking a pointy soar from legacy enterprise densities. Whereas conventional racks used about 12 kW, AI-ready racks can require 80-120 kW for coaching. For understanding, a single 100 kW AI rack operating 24/7 in India (at ₹8-10 per unit/kWh) would value ₹6-7 lakh per 30 days simply in electrical energy, earlier than cooling or flooring house prices.

Knowledge centres attempt to decrease energy prices by means of a mixture of effectivity, expertise and placement technique. Enhancing Energy Utilization Effectiveness (PUE) can materially reduce vitality payments; a 0.1 discount in PUE can save about ₹10 crore yearly for a 20 MW facility. Operators are additionally utilizing AI to optimise cooling and energy distribution in actual time.

Lengthy-term renewable energy buy agreements (PPAs), too, assist lock in decrease vitality prices. Some States providing electricity-duty waivers or concessional tariffs make sure areas extra enticing.

Knowledge centres are additionally extremely capital-intensive companies, with massive upfront spending. McKinsey analysis exhibits that by 2030, information centres are projected to require $6.7 trillion worldwide to maintain tempo with the demand for compute energy. Knowledge centres outfitted to deal with AI processing hundreds are projected to require $5.2 trillion in capex, whereas these powering conventional IT functions are projected to require $1.5 trillion. This makes financing prices essential.

Debt is an ordinary a part of funding enlargement, whether or not for development, fit-outs or ongoing operations. Curiosity prices can materially have an effect on margins, particularly when operators add capability aggressively earlier than utilisation ramps up. Reported web debt/EBITDA ratios for main operators vary from below two instances for some gamers to above five-seven instances for extra leveraged ones, with international Actual Property Funding Belief (REIT)-like gamers typically within the 3.8-4.4 instances vary. Within the asset-intensive information centre business, depreciation could be a key swing issue. Excessive depreciation within the early years of capability enlargement tends to depress EBIT, ROCE and PAT, however as utilisation improves and revenues scale up, its relative influence normally falls.

Given the expansion potential, the sector is attracting institutional capital from non-public fairness, pension funds, REIT-like automobiles and international strategic companions. In accordance with business estimates, India’s information centre market has attracted almost $94 billion in investments since 2019. For example, Airtel on March 30 introduced a $1-billion funding in its subsidiary Nxtra, which operates 14 massive core information centres and 120+ edge amenities, by Alpha Wave, Carlyle and Anchorage Capital, with Airtel additionally taking part. In November 2025, Tata Group’s TCS partnered with PE big TPG to scale HyperVault, focusing on over 1 GW of AI-ready data-centre capability with investments of as much as ₹18,000 crore (about $2 billion).

Larger conglomerates have additionally unveiled bold plans this 12 months. Adani Group plans to take a position $100 billion by 2035 in renewable-powered, AI-ready information centres, backed by a parallel scale-up in renewable vitality and storage. Reliance has outlined a $110-billion, seven-year AI infrastructure plan spanning gigawatt-scale information centres, a nationwide edge-computing community and AI providers built-in with Jio.

Knowledge centre worth chain

A knowledge centre attracts on a large vendor ecosystem.

The server layer consists of the likes of Dell and Hewlett Packard, whereas networking gear comes from Cisco, Arista Networks and Juniper Networks. {The electrical} spine spans UPS methods, switchgear, energy distribution items (PDUs), with distributors resembling Schneider Electrical, Vertiv, Eaton and ABB. The cooling stack consists of chillers from corporations resembling Johnson Controls, Trane, Provider and Daikin; heat-rejection tools resembling cooling towers, dry coolers and associated methods from SPX Applied sciences, Ebara and Kelvion; and laptop room air handlers (CRAHs) from Vertiv, STULZ and Johnson Controls. Again-up energy comes from suppliers resembling Caterpillar, Rolls-Royce mtu and Cummins. Massive initiatives additionally depend on engineering and design corporations resembling Jacobs, Burns & McDonnell and WSP, together with development specialists resembling Turner, Holder and HITT.

In India, the worth chain spans a number of listed and unlisted gamers. E2E Networks, as a specialised AI-cloud supplier, competes with AWS, Microsoft Azure and Google Cloud. Cooling wants create alternatives for Voltas, Blue Star and Hitachi. The telecom alternative is served by Reliance Jio, Bharti Airtel, Tata Communications and so on. {The electrical} and energy layer is served by corporations resembling Hitachi Vitality India, ABB India, Siemens Vitality, Schneider Electrical and CG Energy, whereas cables/switchgear names resembling Polycab, KEI, Havells are additionally typically cited. Land, shell and real-estate growth contain gamers resembling Brookfield, Blackstone, Embassy and Lodha. Some, resembling Anant Raj, are utilizing their present land banks by means of Anant Raj Cloud to construct AI-ready information centres. Racks, fit-outs and mission execution attract Larsen & Toubro, Sterling and Wilson, NCC and so on.

India has one main benefit within the international race: value. The coverage push can be strengthening. Funds 2026 proposed a 20-year tax vacation, until 2047, for eligible overseas cloud firms utilizing Indian information centres for international operations. This provides to a broader regulatory tailwind from the RBI’s 2018 payments-data localisation mandate, MeitY’s Knowledge Centre Coverage 2020, SEBI’s 2023 data-in-India rule for regulated entities, the DPDP Act 2023 and the IndiaAI Mission 2024.

But India’s enlargement will not be frictionless. A brand new information centre requires near 30 approvals or permissions from Central and State authorities departments earlier than it may possibly begin operations. Land acquisition might be sluggish. Grid connections could take time. Even when India doesn’t face an total nationwide energy scarcity, the provision of dependable electrical energy varies sharply throughout cities and websites. The most important problem could, subsequently, be execution.

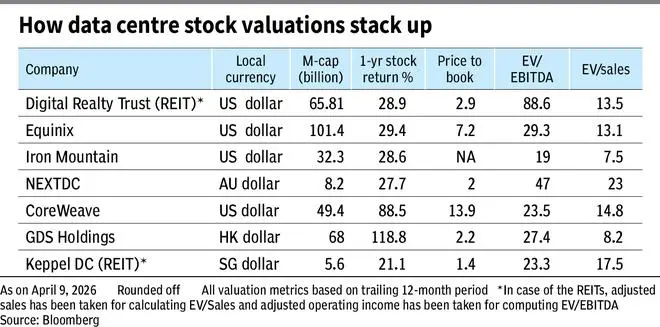

Not like Digital Realty, Equinix, NEXTDC, CoreWeave, GDS Holdings and Keppel DC REIT and so on., not one of the pure-play information centres are listed in India until now. Sify’s information centre enterprise (Sify Infinit Areas) will be the first to record.

Buyers ought to perceive that within the builder-operator mannequin, money flows are back-ended. Operators spend closely on land, energy infrastructure and development lengthy earlier than utilisation matures, so near-term free money stream can look weak even when the underlying asset is enticing. Massive builds might be EBITDA-negative or cash-flow unfavorable till utilisation ramps, which is one motive non-public capital typically dominates the sector. Globally, firms resembling CyrusOne, QTS Realty, Change and Chindata are distinguished examples of knowledge centre corporations that had been as soon as publicly listed however had been later taken non-public.

How one can assess the theme

The professionals for information centre traders are long-duration demand, sticky clients, excessive switching prices and rising worth for power-rich, well-connected campuses. The cons embrace large upfront capital wants, lengthy gestation, execution threat on energy and approvals, and unsure returns if an excessive amount of capability is constructed directly.

A knowledge centre REIT could generate regular rental revenue, however as a result of it distributes most of its money flows, future progress typically needs to be funded by means of contemporary debt, fairness issuance or asset gross sales.

Some traders, particularly in India, may even see the chance as a basic “throughout a gold rush, promote shovels” story. However a listing of “information centre shares” and projected spending will not be an automated option to efficiently trip the increase. Buyers nonetheless want to guage how severely every firm is focusing on the chance in India and abroad, what the administration says on con-calls, whether or not order-wins are translating into income and whether or not margins are enticing sufficient to matter.

For energetic traders, the guidelines ought to fluctuate by phase.

In energy and electrical tools, assess product relevance, execution functionality, order influx, margin profile and aggressive depth.

In cooling, verify whether or not the corporate has real data-centre-grade functionality or is merely utilizing the theme as a story.

In development and fit-outs, examine mission scale, EPC execution, working-capital calls for and margin sustainability.

In telecom and fibre, perceive whether or not information centre demand can materially elevate utilisation and returns.

Throughout all names, traders want to guage whether or not the publicity is actual and scalable, whether or not it may possibly materially enhance income, and whether or not valuations already worth in an excessive amount of optimism.

Printed on April 12, 2026