champc/iStock by way of Getty Photographs

Expensive Companions,

Efficiency and Positioning Overview – Q1 2026

By Q1 2026, McIntyre Partnerships’ outcomes had been roughly -19% gross and -20% web. This compares to our benchmark, the Russell 2000 Worth, which elevated 5%. The fund’s trailing five-year returns are ~12% gross and ~9% web each year, which compares to our benchmark’s return of ~6% each year. Since inception, the fund has returned ~14% gross and ~10% web each year, in comparison with our benchmark’s return of ~7% each year. Our funding in QDEL is a considerably concentrated place, which makes market comparisons much less helpful at current.

McIntyre Partnerships Returns ⁽¹⁾

Within the winners column, CC, ICLR, and SEG contributed 100-500bps. Within the losers column, FTRE, SHC, SWIM, and STHO misplaced 100-500bps, and QDEL misplaced over 500bps.

To state the plain, the Q1 outcome was not a shiny spot for the fund. The first driver of our decline was a pointy pullback within the shares of life science instruments and medical system shares, to which the fund has important publicity, and stock-specific points at QDEL, a life science instruments firm, which I had beforehand known as Inventory A. QDEL is now the fund’s largest place, and we now have collected a full place.

To chop to the chase, I imagine QDEL’s present worth is a once-in-five-to-ten-year alternative. For the third time in ten years, I’ve determined to measurement a place at greater than 20% of the fund’s capital, although we now have bought put choices which restrict our whole loss to underneath 20%. Our two earlier considerably concentrated investments, CC in 2019 and GTX in 2021, additionally concerned massive drawdowns at initiation. They’re additionally our two largest outright winners and drove a 120% gross return from 2020 to 2022, whereas our benchmark elevated solely 14%.

I don’t make this resolution frivolously, and I lay out my considering beneath. If I’m right, I imagine we now have the uncommon alternative for considerably outsized beneficial properties with no lifelike danger of everlasting capital loss. Whereas I’m extremely assured in my evaluation, if I’m incorrect, our funding will end in a big but survivable loss. That is exactly the kind of alternative I search for, and I’m centered and clear-minded as to the potential dangers.

Whereas our present drawdown is uncomfortable, as an investor, I imagine one should often make selections that will look silly within the close to time period to place the fund to generate substantial returns in the long term. I don’t think about the present worth of QDEL rational and don’t have any specific view on the place it’s going to commerce within the close to time period. I care solely in regards to the enterprise’s outcomes and the accuracy of my estimates. These will drive our funding’s success or failure, not the near-term worth motion, which I’ve no means of predicting.

Past QDEL, the fund had blended outcomes. To the upside, CC skilled a big rally, largely attributable to pleasure round its cooling merchandise being utilized in information facilities. SEG rallied modestly as its deal to promote 250 Water Road closed, which, together with the choice to shut the Tin Constructing, has considerably decreased money burn, restructured the stability sheet, and put SEG on a robust footing for fulfillment. We additionally had a profitable commerce in ICLR round its accounting restatement. Whereas I like ICLR’s enterprise and suppose its shares are attractively priced, I didn’t wish to improve our publicity to healthcare, which accounts for over 50% of the fund’s capital, so I exited the place after it partially rallied again. On the dropping facet, SHC and FTRE fell alongside different medical system and life science device corporations. SWIM retrenched with different housing-related equities because the Iran struggle brought on oil costs to surge, which dims the outlook for additional fee cuts. Lastly, STHO fell modestly through the quarter for no specific purpose. STHO is the second largest place within the fund. They not too long ago obtained full compensation from a seller-financed JV and at the moment are in a web money place. STHO has now repurchased ~10% of the shares excellent over the past 12 months, and I anticipate capital returns will speed up now that the JV has been exited.

Portfolio Overview – Exposures and Focus

At month-end, our exposures are 123% lengthy, 27% brief, and 97% web. Adjusted for our choices hedges, the portfolio is roughly 92% web lengthy. Our 5 largest positions are QDEL, STHO, SHC, SWIM, and MDRX, and account for roughly 92% of property.

Portfolio Overview – New Positions

QuidelOrtho Company (QDEL)

Life Science and Diagnostic Instruments Sector

Earlier than I dive into QDEL, I wish to briefly spotlight the general transfer in life science and diagnostics instruments YTD:

The life science instruments house has broadly declined amid fears that AI fashions will dramatically change how medication are developed. I feel we’re a methods away from anybody being injected with a drug made fully from asking ChatGPT with no additional testing, and QDEL particularly has virtually nothing to do with drug improvement, however when blue chip shares in your sector like ABT, TMO, and DHR are all down 15-20%, it is laborious to battle that development.

My level right here is to not preach and make a sector wager, a lot as to level out that neither the January rally in QDEL nor the numerous decline since then is occurring in a vacuum. I don’t suppose AI will essentially exchange something in QDEL’s mannequin any time quickly. If the comp group begins to get better, because the shares are starting to in Might, I feel it’s a favorable backdrop for our funding.

Thesis

QDEL is a healthcare diagnostics instruments firm centered on routine blood testing, primarily at hospitals and central labs, and point-of-care (POC) respiratory testing. Its enterprise is a razor/razor blade mannequin, the place machines are offered or leased up entrance for minimal price (i.e., “the razor”), after which clients commit to buy consumables at excessive gross margins (the “razor blades”). ~95% of gross sales are consumables. Within the labs and immunochemistry companies, which account for over 75% of gross sales, clients signal 5-7-year contracts, and the corporate boasts a >95% contract renewal fee. Given the extremely recurring and non-cyclical nature of their companies, diagnostics corporations usually have >25% EBITDA margins, although particular points have held QDEL at ~22-24% not too long ago.

The essential pitch is that QDEL is a rising, steady enterprise the place one massive situation, the top of the COVID pandemic, has collided with a collection of smaller, largely one-time issues to create a big mispricing. To place the chance in perspective, I feel QDEL can earn ~$4 in 2028 FCF/sh. with 2-3x web leverage. Comparable corporations reminiscent of Siemens Healthineers (SMMNY), ABT, Roche (RHHBY), and DHR all commerce >20x P/E. QDEL is presently buying and selling $11. We will debate multiples, however QDEL shares characterize important worth if the enterprise can return to regular development. A 20x a number of would yield $80.

The numerous mispricing will be defined by the previous expression, “the place there’s smoke, there’s fireplace.” With numerous issues going incorrect unexpectedly, it’s pure for buyers to query whether or not one thing very massive could be going incorrect. I’m sympathetic to this sentiment and perceive why many buyers have put QDEL within the “don’t contact” field. Nonetheless, the problems are primarily impacting QDEL’s respiratory and China divisions, which mixed had been ~25% of 2025 gross sales. Whereas the problems in these two areas are important, the opposite “core” ~75% of the corporate is buzzing alongside fairly properly, rising ~6% in 2025. I imagine these “core” companies ought to earn 2027 revenues of $2.2B and assist a 25% or higher EBITDA margin, yielding ~$550MM in 2027 EBITDA and ~$250MM in totally taxed unlevered FCF (ulFCF). Whereas the corporate has a considerable debt load of $2.5B with ~$170-$200MM in curiosity, on solely the wholesome companies, I imagine we’re paying ~6x EV/EBITDA and ~13x EV/ulFCF, a considerable low cost to comparable growth-rate life sciences and diagnostics corporations that commerce at >10x and >20x, respectively. Additional, whereas troubled, the respiratory and China companies are price “one thing.” Even an excessively conservative 1x EV/Gross sales a number of would yield ~$730MM, or the corporate’s total present market cap. Nonetheless, slightly than one thing that finally ends up offered in a fireplace sale, I imagine administration has a robust plan to show round respiratory gross sales, and the headwinds in China are manageable.

Concerning the draw back, the corporate is levered ~4.1x at current, which I think about excessive however manageable given the extremely recurring mannequin. QDEL not too long ago refinanced its debt, with no maturities earlier than 2030. QDEL generated ~$600MM in 2025 EBITDA and expects ~$615-$630MM in 2026, versus $170-$200MM in curiosity and $130-$150MM in capex, with upkeep capex nearer to $100MM. Its Time period Mortgage B at the moment trades at par. Whereas levered, I imagine QDEL has ample capability to cowl its curiosity prices and is proactively pivoting its respiratory enterprise for future success.

Additional, beneath the floor, I imagine QDEL has a number of strategic levers it could possibly pull. First, QDEL has a captive leasing enterprise that’s at the moment a big drag on FCF, which might be unwound to spice up near-term money move. In 2025, QDEL leased ~$170MM of devices to clients. If, as an alternative, these devices had been offered to clients at a 35% gross margin and a 3rd get together supplied the financing, it might end in a ~$250MM swing in pre-tax money flows. Whereas we perceive administration’s argument that the captive leasing enterprise is a vital gross sales device, QDEL retains the choice to pursue third-party financing, and the $250MM potential swing in money flows offers a considerable buffer versus their $170-$200MM in curiosity prices. Second, the corporate may be break up up or divisions offered to pay down debt, which offers a substantial margin of security that’s not seen at first look. For example, its immunohematology enterprise was rumored to be on the market in 2023, with an estimated worth of $1.5-$2.0B. Since 2023, the section has grown by ~10%, and its development fee has accelerated. Assuming a 25% standalone EBITDA margin and a 12x a number of, consistent with comparable transactions, yields ~$1.7B. Lastly, the corporate has ~$1B of leased gear held on its stability sheet. On condition that QDEL’s clients are a diversified group of hospitals, labs, and medical doctors’ workplaces, I imagine this collateral is good for an asset-backed mortgage. Mixed, I imagine QDEL has sufficient functionality to fulfill its obligations, and the corporate retains substantial flexibility to handle maturities.

The 5 Large Points

I imagine there are 5 distinct points impacting QDEL that buyers should perceive to spend money on the corporate: the decline in COVID testing since 2023, the corporate’s ERP implementation failure, flu seasonality, the Chinese language authorities’s reimbursement charges, and the earnings drag from the launch of QDEL’s next-generation respiratory product. 5 scary-sounding, dangerous issues are rather a lot to deal with, however I imagine every is comprehensible and manageable if one does the work. This complexity is exactly the supply of the chance, and I imagine resolving these points over the subsequent two years will drive a big reweighting of QDEL shares.

I dig deeper within the following sections, however as an preliminary sniff check, I wish to level out how unrelated these 5 points are. Does anybody actually suppose that physician visits within the USA for flu, which fell roughly 30% in Q1, are associated to Chinese language reimbursement charges for ldl cholesterol and HIV testing? Equally, does the associated fee to decommission a plant have something to do with bill timing following an ERP implementation? I might argue not.

I evaluate this to a coin-flipping contest the place tails has come up 5 instances in a row. The percentages of that occurring are about 3%. It is uncommon, but it surely inevitably occurs generally. If, after 5 consecutive tails flips, an odds maker costs the chances of heads at 10:1, and allows you to flip as a lot as you need, you need to take that wager. That is precisely how I imagine QDEL is priced now.

COVID Gross sales Decline and Restructuring

The biggest driver of QDEL’s volatility within the final 5 years is the substantial development and subsequent collapse of QDEL’s COVID testing enterprise. QDEL was the primary firm to enter the market with a speedy antigen COVID check in 2020. Because of this, QDEL gross sales went from $534MM in 2019 to ~$1.7B in 2020 and 2021, with EBITDA growing from ~$158MM to ~$1B in 2020 and 2021, respectively. QDEL used the earnings from the COVID windfall, together with its shares, which elevated 5x in worth, to buy OrthoClinical in 2022, which now makes up QDEL’s Labs and Immunohematology segments and drives ~75% of the corporate’s gross sales. Nonetheless, since 2022, QDEL’s COVID gross sales have collapsed, falling ~95% in three years. Additional, because of the gross sales decline, QDEL has incurred important restructuring expenses because it closes capability it constructed to serve the COVID finish market, which has weighed on FCF. Mixed with the exit of the donor screening enterprise, QDEL’s gross sales and earnings have appeared erratic, risky, and in decline for 3 years. Nonetheless, beneath the floor, QDEL’s non-COVID and DS companies have been constantly rising.

As a thought experiment, if I advised you in 2019 that, within the subsequent two years, our earnings and share worth would surge ~5x, and we’d get to make use of our money generated and the inflated share worth to buy a steady enterprise that was 3-4x bigger than we had been in 2019, I feel everybody would bounce for pleasure. If I additional caveated my prediction and mentioned that we’d then see the enterprise return to regular over the subsequent three years, however we’d lose ~10% of the cash we made on the peak to shut the vegetation we constructed, I feel virtually everybody would nonetheless be excited. Nonetheless, three years of decline and money restructuring expenses are an eternity within the public markets, and QDEL’s shares have lagged because of this.

Whereas QDEL has subsequently run into three distinct, smaller points since Q3 2025 which have additional dropped its share worth, the core of my thesis is that the decline in COVID earnings represents the overwhelming majority of the issues since 2022, when QDEL shares traded over $100, and the core companies have been executing nicely within the background. As COVID gross sales are now not materials, QDEL can return to development, and shares characterize substantial worth.

ERP Implementation

Since fall 2025, QDEL has confronted three distinct points impacting its inventory worth, the primary of which is ERP implementation points in Q3. After the merger with Ortho, QDEL considerably elevated the complexity of its operations, as legacy QDEL primarily focused POC settings by way of distributors, whereas legacy Ortho focused hospitals and central labs by way of a direct gross sales drive. The corporate operates in over 100 nations globally. The choice was made to centralize operations and implement a brand new ERP system. ERP implementations are notoriously sophisticated; Gartner estimates that nearly 75% of them are available in above price and delayed. QDEL’s ERP implementation started following the 2022 merger, with many of the heavy lifting in 2024 and H1 2025, and incurred ~$100MM in money prices that weighed on FCF.

Regardless of the corporate’s greatest efforts, after the system went reside, QDEL initially had problem accumulating its accounts receivable. A/R elevated considerably from $295MM and $282MM and in Q3 and This autumn 2024 to $387MM and $417MM in Q3 and This autumn 2025. This resulted in QDEL lacking its 2025 FCF steerage, with adjusted FCF at ~17% of EBITDA, beneath its 25% goal. Nonetheless, excluding the A/R miss, QDEL would have exceeded its FCF targets. In a vacuum, I don’t suppose many buyers could be significantly involved with bill timing from hospitals, however given the sentiment in QDEL’s shares, the miss solely added gasoline to the narrative that “one thing” is incorrect at QDEL. Additional, in Q1, QDEL efficiently recovered roughly half of the rise in A/R, and I count on them to totally get better A/R inside the subsequent yr. Whereas I perceive the narrative round QDEL’s money technology, I think about the A/R miss explainable and within the rear view.

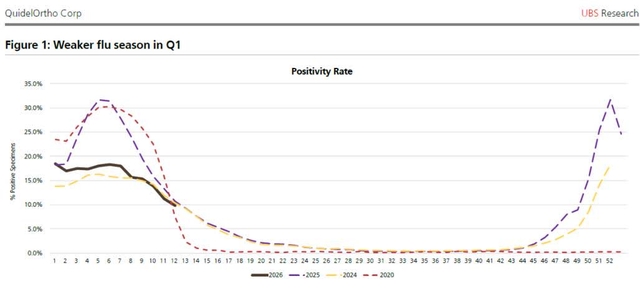

Flu Season

Supply: CDC, UBS, up to date as of April 7, 2026

The second non-COVID situation affecting QDEL was a considerable miss in Q1 2026 flu revenues. Previous to its success with COVID, QDEL’s largest enterprise was the Sofia platform, a broadly distributed POC device

primarily used to check for flu A and B. As I’m certain nobody might be shocked to learn, the flu is extremely seasonal and troublesome to foretell. Following a robust flu season (dangerous for humanity however good for flu testing volumes), the 2025/2026 flu season once more appeared sturdy, and QDEL reported flu revenues up 6% in This autumn 2025. Nonetheless, the flu season unexpectedly fell sharply in Q1, with physician visits for flu signs down ~30% y/y, which drove a ~46% decline in QDEL’s Q1 flu revenues. I attribute the miss relative to physician visits largely to channel fill points and a slight share loss, which I tackle within the LEX part beneath.

Once more, just like the A/R miss, I wish to emphasize that I feel the massive flu miss is attributable to the flu’s inherent volatility and is one-time in nature. Traditionally, a weak flu season is usually adopted by a robust one. Additional, identical to the A/R miss, I feel most buyers perceive this and could be inclined to present QDEL a move, had been it not for the narrative and repeated misses relative to prior expectations. It’s these stacked one-time points which have brought on the dislocation. I count on that as these aberrations reverse and return to regular, QDEL’s shares can improve.

China Reimbursement Coverage

The ultimate of QDEL’s three one-time points is the Chinese language authorities’s change in reimbursement charges for its product. Whereas the coverage is just not but finalized, it’s already affecting QDEL’s China revenues, which fell by ~15% in Q1 as distributors pulled again in anticipation of the proposed pricing change. Of the three points, I think about the China information an actual destructive, and whereas I used to be conscious it might happen, it barely lowers my upside in comparison with once we started buying shares within the fall. It is very important be aware that modifications in Chinese language reimbursement insurance policies have been hitting most gamers within the diagnostic house, with DHR, Roche, ABT, and so on., all experiencing points. I additionally argue that it’s largely exterior of administration’s management, although their execution of cost-outs following the decline is essential.

The change in China’s coverage can be probably the most troublesome situation to mannequin, as we nonetheless have no idea how, when, or what the precise coverage might be. Nonetheless, given the repeated issues in China, I feel considerably decreasing my estimates for China is logical, and I fully exclude the China section from my ~$550MM in core 2027 EBITDA projection. In 2025, the China section had $334MM in gross sales and $141MM in EBITDA, although QDEL runs a big ~$600MM company section that possible consists of $30-$50MM in prices largely attributable to the China enterprise. Administration has mentioned the rule change ought to impression roughly half the enterprise, with a 30-40% haircut potential. For conservatism, I mannequin it as a $70MM EBITDA hit, with the impression felt virtually fully within the subsequent 18 months. Whereas materials, I mannequin QDEL’s core EBITDA at $550MM in 2027 earlier than any contribution from China or respiratory gross sales, thus I think about the China points manageable, albeit disappointing.

LEX Launch and 2026 Earnings Drag

Lastly, one of the crucial underestimated elements of the story is the launch of LEX for 2 causes: the chance is substantial, however it’s at the moment a ~$50MM drag on earnings because the product doesn’t launch in earnest till 2027. LEX is a next-generation POC device for molecular diagnostics testing, initially focused at COVID and flu A/B. As talked about earlier, I imagine QDEL’s flu enterprise is modestly dropping share, and at the very least a part of that loss is to rival molecular diagnostics rivals, reminiscent of Abbott’s ID NOW and DHR’s GeneXpert. For instance, QDEL estimates that 90% of its Sofia clients are at the moment additionally utilizing molecular diagnostic instruments. To place LEX’s device in perspective, it offers a constructive end in underneath six minutes and a destructive end in underneath ten, in contrast with 15 to half-hour for older molecular instruments. Whereas real-world accuracy and pace can differ from what’s marketed, I imagine LEX has a robust probability of turning QDEL’s respiratory enterprise again right into a development engine. QDEL sizes the molecular respiratory market at ~$3B, and even 5% market share could be a big enhance to its $400MM in 2025 respiratory gross sales.

Additional, I imagine the market is underestimating the cash-flow drag from the launch of LEX. Whereas administration has not supplied a lot element, they beforehand estimated the canceled Savanna platform as a ~$50MM drag on margins, or 200bp, with half reallocated to LEX, and sure extra in 2026 given its anticipated ramp into 2027. This ends in QDEL’s anticipated margin ramp from 22% final yr to >25% in H2 2027 showing steeper than it truly is. I imagine QDEL is already working at near a 25% margin, excluding the LEX launch. As LEX rolls out in H2 2026, it’s going to include excessive incremental margins, and I imagine QDEL will meet its 2027 margin targets.

Important Focus Philosophy

Lastly, I want to remind buyers of our concentrated place philosophy. When the partnership made our first considerably concentrated funding in 2019, I wrote an inventory of standards that I imagine any concentrated place should meet. These are our guardrails for taking over such a big funding. I wish to remind companions of those guardrails and briefly clarify why I imagine QDEL meets them.

For a considerably concentrated funding, I’m searching for:

• Deep Moat/Predictable Money Flows – Whereas the phrase “deep moat” is commonly thrown round, what I imply by a “deep moat” is a enterprise with sturdy aggressive positioning that makes long-term money move predictable. I would like investments the place I’m extremely assured that it might be troublesome for my long-term estimates to be considerably incorrect. The overwhelming majority of companies don’t meet this criterion, or at the very least I don’t imagine I’m able to analyzing them with such certainty. Single product medtech/pharma, development investments with out near-term money flows, swing commodity producers, and so on. come to thoughts.○ QDEL Rationalization: ~75% of gross sales are its core lab testing and immunohematology practices, that are razor/razorblade fashions with excessive switching prices, 5–7-year contract phrases, 95% of revenues from recurring consumables, and a >95% buyer renewal fee. QDEL can be presently gaining market share. • Enough Liquidity in Any Setting – A lot of issues can go incorrect on the planet, from macro crises to plant fires to poor enterprise selections, which may trigger a world of bother for a enterprise that should entry the monetary markets. I’m solely prepared to take a position substantial capital in companies the place liquidity is a non-issue.○ QDEL Rationalization: Whereas ~4x levered, the corporate renegotiated its time period mortgage within the fall, the debt is just not due till 2030, they’re in compliance with all covenants, and QDEL retains substantial levers, reminiscent of promoting a division or exiting its capital-intensive leasing enterprise, which might be used to scale back debt • Clear Differentiated View (For Liquid Securities) – In a liquid safety, there are prone to be a couple of points which the market perceives as massive dangers. I should have a robust view on these and have to be satisfied that the end result of those points is knowable and considerably totally different than the market expects. This might not essentially apply to extremely illiquid securities, the place lack of investor data generally explains the chance.○ QDEL Rationalization: I imagine the market is incorrectly viewing QDEL as extremely unpredictable because of the 5 concurrent points, slightly than a extremely predictable franchise offering routine medical diagnostics at hospitals and labs • Affordable Development (Or Very Gradual Decline) – When shopping for a deeply discounted safety (i.e. underneath 5x run-rate homeowners’ earnings), we don’t want speedy development. Nonetheless, we’re very cautious concerning companies in secular decline and would keep away from them normally.○ QDEL Rationalization: Excluding respiratory gross sales, QDEL has constantly grown revenues at a mid-single digit fee for the final 5 years • Substantial Upside – I’m solely interested by important focus the place we stand to make an excessive amount of cash, or a modest amount of cash in a short time. One thing like a larger than 50% IRR sounds proper.○ QDEL Rationalization: I imagine QDEL is price at the very least 15x my 2028 estimate of $4, or $60 per share. Assuming a 2.5 yr holding interval yields a 97% IRR. • Affordable Timeframe to Work – As at all times, timing is an informed guess, and I’ll often be incorrect. Nonetheless, I would like our huge bets to have an inexpensive timeframe – suppose a couple of quarters, not a couple of years.○ QDEL Rationalization: I imagine QDEL inventory can considerably reweight this yr because it generates constructive FCF in H2 2026 and China finalizes rule-making • Catalysts – Associated to timeframe, I ought to have cheap near- and medium-term catalysts for our funding.○ QDEL Rationalization: I imagine our largest catalysts over the subsequent 12 months are China finalizing reimbursement charges, constructive FCF in H2 2026 and FY2027, and a reduction rally in life science instruments as AI fears show unfounded • Technical or Panic Promoting – That is admittedly an arbitrary idea, however ideally, I want to be shopping for from technical or panicked sellers who’re worth detached.○ QDEL Rationalization: Following the Q1 2026 pre-announcement, QDEL fell >30% in a day, and roughly 40% of shares excellent modified arms within the following week • No Actual Potential for Everlasting Capital Loss – That is by far the one most essential criterion. My evaluation ought to embody not simply basic dangers, like macro, but additionally tail dangers. Nonetheless, I have to be centered on believable tail dangers. For example, a plant fireplace is a believable tail danger; three simultaneous plant fires at three separate vegetation on three totally different continents is just not. This may at all times be a subjective judgment, however I have to be satisfied it’s true.○ QDEL Rationalization: Finally, this can be a judgment name. The corporate offers mission-critical lab gear to hospitals underneath lengthy contracts and is presently rising MSD, excluding respiratory. The Ortho division has been acquired at 11x and 14x EBITDA beforehand, but shares indicate a sub-5x valuation. The combination of predictability, important money technology when correctly analyzed, and debt flexibility provides me confidence that our odds of everlasting capital loss are successfully zero. Additional, we’re hedged to restrict losses even when this state of affairs performs out.

As at all times, please be happy to contact me with any questions.

Sincerely,

Chris McIntyre

References

(1) The returns offered on web page 1 from January by way of August 2017 characterize the efficiency outcomes of a private proprietary buying and selling account managed by the Founder with a method much like the technique of the Fund. All web returns are calculated utilizing a 1.5% administration price, 20% incentive price, and 5% laborious hurdle. Returns are topic to future adjustment and revision.

Authentic Put up

Editor’s Be aware: The abstract bullets for this text had been chosen by Searching for Alpha editors.