Shares of Greenback Common Company (NYSE: DG) rose over 6% on Friday. The inventory has gained 76% year-to-date. The low cost retailer chain delivered strong outcomes for the third quarter of 2025 and raised its steering for the complete yr. The corporate continues to realize traction on its initiatives and stays optimistic on its progress alternatives.

Robust Q3 efficiency

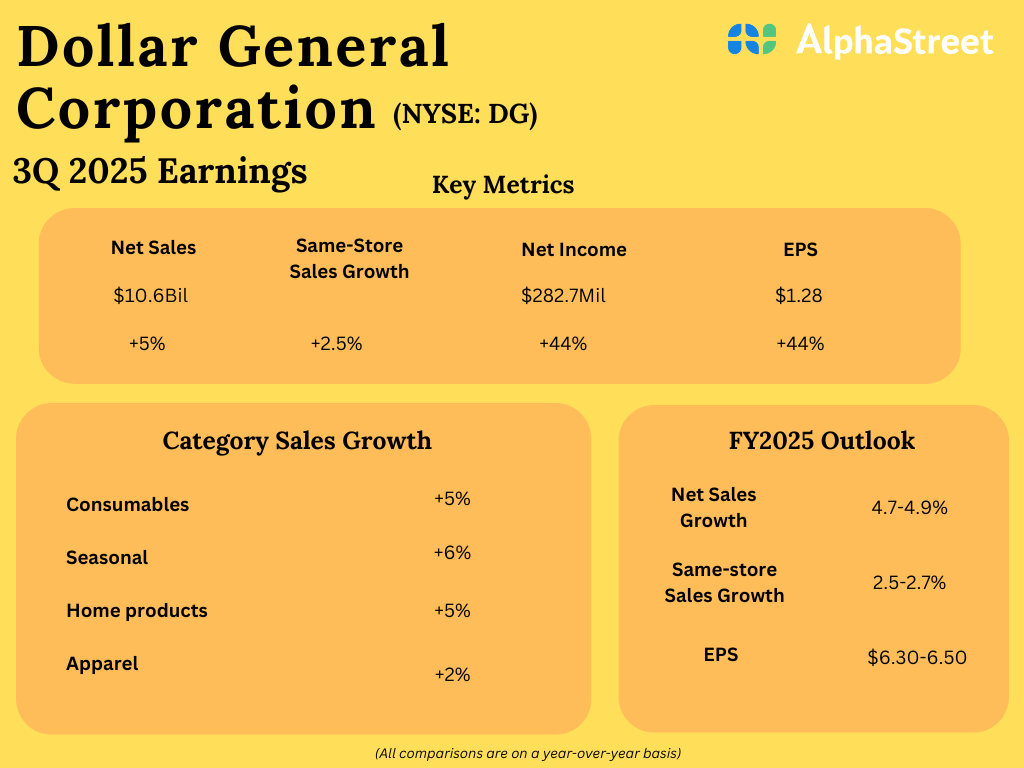

In Q3 2025, Greenback Common’s web gross sales elevated 4.6% year-over-year to $10.6 billion, pushed by same-store gross sales progress and optimistic contributions from new shops. Identical-store gross sales grew 2.5%. Web revenue rose 43.8% to $282.7 million, or $1.28 per share, in comparison with final yr.

Robust worth proposition

Greenback Common continues to profit from its wide selection of choices that present worth to clients. In Q3, the corporate noticed a 2.5% progress in buyer visitors whereas the typical transaction quantity remained flat. As talked about on its quarterly name, the greenback retailer continues to realize extra clients, particularly from higher-income households. By its various assortment and low value factors, DG believes it could achieve market share with clients throughout all revenue teams.

In the course of the third quarter, Greenback Common noticed gross sales and comps progress throughout all its classes – consumables, seasonal, residence, and attire. It gained market share in each the consumables and non-consumables classes.

Development initiatives

Greenback Common is specializing in quite a few initiatives to drive progress, which embrace its actual property tasks and digital capabilities. The corporate continues to revamp its retailer fleet via new retailer openings and remodels. Its transform applications Undertaking Renovate and Undertaking Elevate are seeing substantial progress.

Within the third quarter, DG opened 196 new shops, and transformed 651 shops via Undertaking Elevate and 524 shops via Undertaking Renovate. The corporate believes it’s well-positioned to serve clients in rural areas of the US, with 80% of its present retailer base serving small cities. Wanting forward, DG plans to open larger-footprint shops primarily in rural communities, with an expanded vary of choices that may provide worth and comfort to clients.

Greenback Common’s digital initiatives complement its huge retailer footprint, and its cellular app and web site are common with clients. Its DG Supply service and its partnerships with DoorDash and Uber Eats are serving to enhance its supply capabilities. The corporate is seeing bigger basket sizes and robust repeat go to charges from clients on its supply platform, with ample alternative for gross sales progress.

Upbeat outlook

Greenback Common raised its steering for fiscal yr 2025, primarily based on its robust Q3 efficiency and an improved outlook for the rest of the yr, whereas additionally preserving in thoughts the unsure client atmosphere. The corporate now expects web gross sales progress of 4.7-4.9%, same-store gross sales progress of two.5-2.7%, and EPS of $6.30-6.50 for the yr.